Precious Metals Market Manipulation

What actually sets the gold price

The gold price quoted on this site, and on every financial ticker, is not set by people buying and selling gold. It is set by traders exchanging contracts, most of which will never be settled in metal.

The contract that matters most is the COMEX gold future. COMEX is the Commodity Exchange, a division of CME Group, and a single gold futures contract is a standardised agreement to buy or sell 100 troy ounces of gold, of no less than 995 fineness, at a set price on a set future date. The contract can in theory be settled by delivering physical metal: during the delivery month a seller issues a delivery notice, and gold is transferred between COMEX-approved vaults, usually as a book entry rather than a physical movement.

In practice that almost never happens: fewer than 1% of COMEX gold futures contracts result in physical delivery, and the rest are closed out before the delivery month arrives. Positions are settled in cash twice a day, with gains and losses moving between margin accounts as the price moves and no metal changing hands.

This is where the spot price comes from. The most actively traded COMEX contract, usually the nearest delivery month, serves as the reference, and the spot price is that futures price adjusted for the small carrying cost between now and delivery. A primer on COMEX futures states it plainly:

"When you see 'gold is trading at $X per ounce,' that price is typically derived from the most active COMEX gold futures contract."

London runs the other half of the system. The London Bullion Market Association oversees an over-the-counter market where most of the world's gold and silver trades by value, in bilateral deals between banks rather than on a public exchange. The scale is large: the London clearing system alone moved 17.9 million ounces of gold, about $87 billion, in February 2026. Twice each day the LBMA also publishes a benchmark, the LBMA Gold Price, which dealers and contracts worldwide reference. That benchmark is the successor to the London Gold Fix, a twice-daily price that ran from 1919 until 2015.

Both venues trade claims on gold rather than gold itself, and physical metal is priced off them. Because the paper markets are so much larger and more liquid than the trade in actual coins and bars, price discovery happens there. A large sell order in the New York futures market can move what a buyer in London pays for a bar that is already sitting in a vault.

The number on a bullion dealer's website, including this one, is that paper price. It is the infrastructure that produces the gold price, and everything that follows in this guide is about what has been done to it.

The banks that admitted to rigging gold

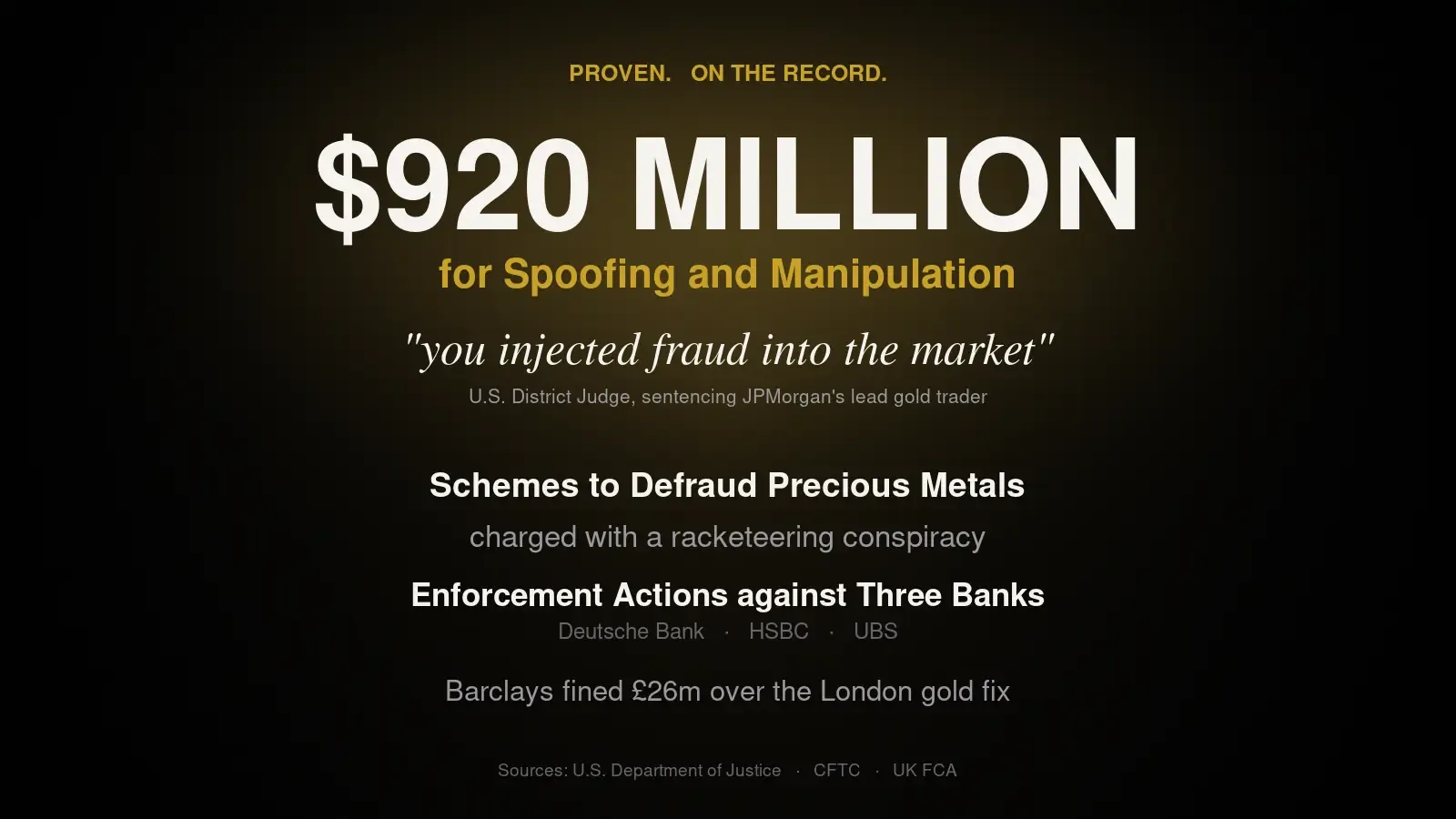

Eight banks have paid more than $1.3 billion in fines for manipulating the gold and silver markets, and several of them admitted it. JPMorgan admitted to wire fraud. Scotiabank admitted to lying to its regulator. Traders were convicted by federal juries and sent to prison. This is the documented record, drawn from court filings, regulatory orders, and the traders' own messages.

The conduct ran for roughly a decade, from 2007 to 2016, across desks in New York, London, Singapore, and Hong Kong. It was prosecuted by the United States Department of Justice, penalised by the Commodity Futures Trading Commission, and in one case fined by the United Kingdom's financial regulator. Much of the evidence is the traders' own chat logs, entered as exhibits in open court.

Spoofing: what it is

Spoofing moves a price with orders the trader never intends to fill. A large order to buy or sell is placed, big enough to convince the rest of the market that supply or demand has shifted. Other participants and their algorithms react, the price moves, and the fake order is cancelled before it can execute. The profit comes from a smaller, genuine order resting on the other side, which gains from the move the fake order created.

On COMEX, the New York exchange where gold and silver futures trade, JPMorgan's traders did this hundreds of thousands of times. The traders described the tactic in their own words. One Bank of America trader wrote that it "does show you how easy it is to manipulate it sometimes" and added, "I know how to 'game' this stuff." A colleague wrote, "I just put in 500 lots to spoof the gold," and, "if you spoof this it really moves." A Deutsche Bank trader, James Vorley, put it plainly: "This spoofing is annoying me. It's illegal for a start."

The silver desks worked across banks. Deutsche Bank's records, later handed to investigators, captured a UBS trader writing that "u can easily manipulate silver" and a Deutsche Bank trader answering "today u smash." These were not stray remarks. They were routine descriptions of how the desks operated, written by the people operating them.

The convictions

JPMorgan paid $920 million in September 2020 to settle the spoofing case, the largest penalty the CFTC had imposed to that point. The bank entered a deferred prosecution agreement and admitted to two counts of wire fraud. Federal prosecutors had charged the precious metals desk under the racketeering statute written for organised crime, and Bloomberg reported the government's position that the desk "was a criminal enterprise." Between 2008 and 2016, traders on that desk placed hundreds of thousands of orders they intended to cancel.

Three JPMorgan traders were convicted at trial. Michael Nowak, the head of the global precious metals desk, and Gregg Smith, its top gold trader, were found guilty in August 2022 of wire fraud, commodities fraud, attempted price manipulation, and spoofing; the jury acquitted them of the racketeering charge. Smith, described by a prosecutor as "the most prolific spoofer that the government has prosecuted to date," received two years in prison. Nowak received a year and a day. Two more traders, John Edmonds and Christian Trunz, had already pleaded guilty and cooperated; Trunz testified that spoofing "was an open strategy on the desk. It wasn't hidden."

"You told many lies to the market. For many years, you injected fraud into the market."

Deutsche Bank settled first and then turned on the others. In 2016 it paid $38 million to settle silver-rigging claims and $60 million over gold, and agreed to cooperate with the plaintiffs suing the remaining banks. It handed over more than 350,000 documents and 75 audio recordings, which the plaintiffs called the proof of a coordinated conspiracy. Two Deutsche Bank traders, James Vorley and Cedric Chanu, were later convicted of wire fraud, and the Supreme Court declined to hear their appeal in 2023. A separate CFTC order added $30 million.

Scotiabank paid about $128 million and left the business entirely. Four of its traders had spoofed gold and silver futures for years, and the bank then made false statements to the CFTC about it, drawing a record $17 million penalty for the false statements alone. The CFTC found that "senior compliance members possessed substantial information about unlawful trading but took no appropriate action." Scotiabank shut its metals unit, ScotiaMocatta, and gave up its seat at the London fix.

Merrill Lynch, owned by Bank of America, paid about $50 million in 2019, and two of its senior traders, Edward Bases and John Pacilio, were convicted in 2021. UBS ($15 million), HSBC ($1.6 million), and Morgan Stanley ($1.5 million) settled spoofing cases with the CFTC. Not every prosecution succeeded: a jury acquitted the UBS trader Andre Flotron in 2018, the first acquittal in a criminal spoofing case since the practice was outlawed in 2010.

| Bank | Penalties | Years |

|---|---|---|

| JPMorgan Chase | $920 million | 2020 |

| Deutsche Bank | about $232 million | 2016-2021 |

| Scotiabank | about $128 million | 2018-2020 |

| Merrill Lynch (Bank of America) | about $50 million | 2019 |

| Barclays | £26 million (about $44 million) | 2014 |

| UBS | $15 million | 2018 |

| HSBC | $1.6 million | 2018 |

| Morgan Stanley | $1.5 million | 2019 |

This was not the work of one rogue trader. More than ten traders across eight banks were convicted or pleaded guilty, and seven were sent to prison, for spoofing gold and silver between 2007 and 2016.

The London gold fix

For most of a century, the global price of gold was set twice a day by a handful of banks on a phone call. The London gold fix began in 1919, and by the time it ended in 2015 five banks ran it: Barclays, Deutsche Bank, HSBC, Scotiabank, and Societe Generale. Twice each day they compared their clients' buy and sell orders and moved a proposed price up or down until the orders balanced. The figure they agreed became the reference price used by miners, refiners, jewellers, and central banks worldwide.

The design handed the members an advantage no outsider had. During the call, each bank could see which way the order flow was running before the price was published, and nothing stopped them from trading on that knowledge in the open market at the same time. No regulator listened in, and no transcript was published. Five firms set a price that everyone else had to accept, and they set it among themselves.

Two academic studies found the fix behaving as that design would predict. In 2014, Andrew Caminschi and Richard Heaney examined trading around the afternoon fix and found that trades placed in the first five minutes of the call correctly predicted the final price direction about 80% of the time, against 50% for trades placed beforehand. The information was leaking out before the price was announced. By the time the result was published, the market had already moved.

A second study went further. Rosa Abrantes-Metz of NYU Stern, whose earlier work had helped expose the LIBOR scandal, examined intraday gold prices from 2001 to 2013 with Albert Metz of Moody's. They found sharp price moves clustered at the afternoon fix that did not appear at the morning fix and had not occurred before 2004. In six separate years the large moves ran downward more than two-thirds of the time, and in 2010 they ran downward 92% of the time. The structure of the benchmark, the authors wrote, was "certainly conducive to collusion and manipulation," and the data were "consistent with price artificiality."

One trader was caught in the act. On 28 June 2012, a Barclays director named Daniel Plunkett placed a large sell order into the afternoon fix, withdrew it about a minute later, then placed another, driving the price below $1,558.96. That barrier mattered: if gold fixed above it, Barclays owed a client a $3.9 million payout. The price fixed below it, Barclays avoided the payout, and Plunkett's own book gained $1.75 million. The client noticed the move and complained. The FCA fined Barclays £26 million, banned Plunkett from the industry, and found that the bank's failure to control fixing conflicts had run from 2004 to 2013.

The class-action lawsuits that followed turned up more. Deutsche Bank's settlement evidence exposed traders at several banks coordinating their moves and naming themselves for it. They called their group a "mafia" and recruited others into it; "Ok calling barx," one wrote, meaning Barclays. They called themselves the "stop busters" for driving prices to the levels where clients' automatic stop-loss orders would trigger. The gold-fix class action eventually settled for about $152 million, with Deutsche Bank the first to pay and HSBC, Barclays, Scotiabank, and Societe Generale following.

The silver fix collapsed first. Deutsche Bank quit it in early 2014 and could not find a buyer for its seat; the last silver fixing took place on 14 August 2014, ending a benchmark that had run for 117 years. The gold fix lasted until March 2015, when it was replaced by an electronic auction run by an arm of the Intercontinental Exchange and regulated by the FCA. The new auction kept the same two daily times, and several of the banks that paid fines for metals manipulation sit on the panel that runs it.

In January 2014, the president of Germany's financial regulator, Elke Koenig, said precious metals manipulation was more serious than the LIBOR scandal, because metals prices are based on real transactions rather than the estimates banks submitted for LIBOR. She said it the day before Deutsche Bank announced it was leaving the gold and silver fixings.

The pattern across markets

The banks that rigged the metals markets are the same banks that appear in nearly every other financial scandal of the era. Every major bank fined for precious metals manipulation was also caught rigging LIBOR, the interest rate benchmark that underpinned hundreds of trillions of dollars in contracts. Deutsche Bank paid $2.5 billion over LIBOR, UBS $1.5 billion, JPMorgan $550 million, and Barclays more than $400 million; total LIBOR fines across all banks ran past $8.5 billion. The mechanism was the same as the fix, a small group of banks submitting the numbers that set a global benchmark and adjusting them to suit their own positions.

The record extends past market-rigging. JPMorgan paid $290 million to settle claims it served as banker to Jeffrey Epstein's operation, plus $75 million to the U.S. Virgin Islands; Deutsche Bank paid $75 million to Epstein's victims and a $150 million regulatory penalty over the same accounts. HSBC admitted in 2012 to laundering at least $881 million for the Sinaloa and Norte del Valle drug cartels, paying about $1.9 billion. A Congressional report later titled "Too Big to Jail" found that senior U.S. officials had rejected a push to prosecute the bank, and no executive went to prison.

The same risk culture surfaced inside JPMorgan during the spoofing years. In 2012, while the metals desk was running its scheme, a trader in the bank's London office built credit derivatives positions so large that the market nicknamed him the "London Whale." Jamie Dimon dismissed the first reports as a "tempest in a teapot." The losses grew to $6.2 billion, and JPMorgan paid more than $920 million in fines and admitted to violating federal securities law.

The overlap is not confined to one or two firms. The same banks recur across the major financial scandals of the period, through the same years and often under the same management.

| Bank | Precious metals | LIBOR | Other |

|---|---|---|---|

| JPMorgan | $920M spoofing (2020) | $550M | Epstein settlements $365M (2023); London Whale, $6.2B loss (2012) |

| Deutsche Bank | $30M spoofing plus gold and silver fix settlements | $2.5B | Epstein settlements $225M (2020-2023) |

| HSBC | $1.6M spoofing; sets the London gold price | part of the scandal | $1.9B cartel money laundering (2012) |

| UBS | $15M spoofing (2018) | $1.5B | FX manipulation |

| Barclays | £26M gold fix (2014) | $400M+ | FX manipulation |

HSBC paid its $1.9 billion money-laundering penalty and kept its place in the gold market. It remains one of the banks that sets the daily London gold price. The banks are not the only force with an interest in the price of gold; the governments that oversee them have spent decades trying to hold it down.

Why governments fight the gold price

The officials who ran these currencies have said, on the record, that gold is the real money and that central banks act to manage its price. Alan Greenspan chaired the Federal Reserve for nineteen years. In 1966, long before he took the job, he wrote that "in the absence of the gold standard, there is no way to protect savings from confiscation through inflation." In October 2014, years after leaving it, he told the Council on Foreign Relations: "Gold is a currency. It is still by all evidences the premier currency where no fiat currency, including the dollar, can match it."

His most consequential remark on gold, he made in office and under oath. Testifying to the House Banking Committee on 24 July 1998, defending the loose regulation of derivatives, Greenspan told Congress that gold could not be cornered because "central banks stand ready to lease gold in increasing quantities should the price rise." Gold traded near $290 an ounce that summer. The chairman of the Federal Reserve had told Congress, as reassurance, that the central banks would put gold into the market to stop its price rising.

Paul Volcker, who chaired the Fed before Greenspan and helped close the gold window as a Treasury official in 1971, was blunter in his memoirs. Recalling February 1973, he wrote: "Joint intervention in gold sales to prevent a steep rise in the price of gold, however, was not undertaken. That was a mistake." The regret is precise. The central banks should have sold gold together to hold its price down, and not doing so was, in his account, an error of policy.

The most explicit statement came from the Bank of England. Eddie George, its governor from 1993 to 2003, spoke with Nicholas Morrell, the chief executive of the mining company Lonmin, in the autumn of 1999, after the gold price jumped and banks holding short positions rushed to cover. The scramble led to the Washington Agreement, in which central banks capped their gold sales. George's explanation of what drove them left little room for reading between the lines.

"We looked into the abyss if the gold price rose further. A further rise would have taken down one or several trading houses, which might have taken down all the rest in their wake. Therefore at any price, at any cost, the central banks had to quell the gold price, manage it."

Mario Draghi led the European Central Bank from 2011 to 2019. Asked about gold at the Harvard Kennedy School in 2014, he described it from the central bank's side: "for central banks this is a reserve of safety... in the case of non-dollar countries it gives you a value-protection against fluctuations against the dollar." The men who ran the dollar, the pound, and the euro each described gold as money, or as something to be held down, or both.

An ounce of gold bought a fine suit of clothes in ancient Rome, and it buys one today. The economist William Bernstein summed up the comparison: gold's real return over two thousand years "appears to be zero: in ancient Rome, an ounce of it acquired a fine toga, and nowadays it acquires a decent man's suit." At around $4,500 an ounce in 2026, gold buys within the range of a bespoke Savile Row suit, where prices run from about £1,600 at entry houses to £4,600 and beyond at Huntsman and Edward Sexton.

The currencies people actually save in have gone the other way. The US dollar has lost about 97% of its purchasing power since the Federal Reserve was created in 1913; a hundred dollars today buys what $2.97 bought then. The British pound has done worse, holding on to just 0.67% of its 1913 value, a fall of 99.3%. In the same span over which gold kept buying the same suit, the dollar and the pound lost almost everything they had.

A rising gold price is the most visible sign that a currency is being inflated. In a 2002 speech, the future Federal Reserve chairman Ben Bernanke described where dollars come from: "The U.S. government has a technology, called a printing press, that allows it to produce as many U.S. dollars as it wishes at essentially no cost." In the same speech he named the condition that gives money its value: "Like gold, U.S. dollars have value only to the extent that they are strictly limited in supply." A climbing gold price is the market reporting that the limit is not being held.

The supply of money

The expansion Bernanke described is measurable. The Federal Reserve's M2 money supply, the broadest common count of dollars in the economy, stood at $286.6 billion in 1959, the first month in the Fed's own series. By April 2026 it had reached $22.8 trillion, a 79-fold increase.

Much of that growth is recent. Between January 2020 and April 2022, M2 grew by about 41% in twenty-seven months, and the stimulus of the COVID period added roughly $6.3 trillion to the money supply in under three years. In those two years the Federal Reserve and the Treasury created about as much new money as had existed in total in 2007.

The economist who became Treasury Secretary

There is an academic account of how a gold price can be held down, and one of its authors went on to run the US Treasury. In 1988, while a professor at Harvard, Lawrence Summers published "Gibson's Paradox and the Gold Standard" with Robert Barsky in the Journal of Political Economy. The paper set out the long historical link between gold, interest rates, and the general price level.

The finding was straightforward. When real interest rates are negative, with rates sitting below inflation, gold rises as savers reach for something that holds its value; when real rates are positive, gold stagnates or falls. Read as policy, it points one way: keep real interest rates high enough and the gold price stays down, with no need to touch the metal. Summers became Deputy Treasury Secretary in 1995 and Treasury Secretary in 1999, heading the department that holds the United States' gold.

How to rig a price with paper

On COMEX, the main United States futures exchange for gold and silver, the paper claims outnumber the metal available to settle them. At the end of May 2026, open interest in silver futures stood at the equivalent of 507.7 million ounces. The silver actually registered for delivery in COMEX vaults was 84.1 million ounces. That is close to six paper ounces for every deliverable one.

A futures contract is what makes the gap possible. One COMEX gold contract represents 100 troy ounces of metal; one silver contract represents 5,000. The holder can carry the contract to expiry and demand bullion, or settle in cash and walk away. Almost everyone does the second thing. Fewer than 1% of COMEX contracts have historically ended in physical delivery, with the rest closed out or rolled into a later month before any bar moves.

The vault numbers come in two categories, and the distinction is where most of the confusion lives. Registered metal carries a warrant and can be delivered against a futures contract. Eligible metal sits in the same approved vaults and meets the same purity standards, but has no warrant and cannot be delivered against a contract unless its owner chooses to register it. Only the registered pile backs the futures market. Reports of record COMEX inventories usually count both piles together.

Set the paper claims against the registered metal and the imbalance is clear. The eligible stock, larger in both metals, does not enter the equation unless its owners decide to make it available.

| Metal | Registered | Eligible | Open interest | Paper claims per registered ounce |

|---|---|---|---|---|

| Gold | 15.6M oz | 12.8M oz | 34.6M oz | 2.2 |

| Silver | 84.1M oz | 232.4M oz | 507.7M oz | 6.0 |

COMEX figures as of 26 to 27 May 2026, via the goldsilver.ai gold and silver trackers. Silver's registered stock covers 16.6% of the open interest standing against it; gold's covers 45.2%. If more than one silver contract in six asked for metal, the registered vault would run dry. The market functions because almost nobody asks.

This is the mechanism. The price quoted on a dealer's website, and on this one, is the futures price, not the price of a specific bar in a specific vault. A large sell order in the futures market moves that quoted price down regardless of whether the seller owns any metal, because the contract is a promise that will almost certainly be settled in cash rather than bullion. A trader who wants the price lower does not need silver. He needs contracts.

The short side belongs to a few banks

The selling is not spread across thousands of hands. Ted Butler, an independent silver analyst, spent more than thirty years documenting how few traders hold the short side of COMEX silver. He first flagged it in the 1990s, when he noticed that open interest in the contract was, in his words, "out of whack with all other commodities."

The Commitments of Traders report, the CFTC's own weekly tally of who holds what, bears the concentration out. In the reporting week of 5 July 2016, the four largest short traders held 68,476 net contracts, the equivalent of 342.4 million ounces of silver, or 32.4% of all open interest. The eight largest held 98,065 contracts net short, 490.3 million ounces, 46.4% of the entire market. Most of those traders were banks, and together the eight held effectively the whole net commercial short position.

No ordinary commodity looks like this. The concentrated silver short ran to more than 200 days of global mine production. The same measure for corn or crude oil came to a few days. The four biggest silver shorts alone stood for roughly 105 days of world production, a position no miner needed for hedging and no normal speculator would carry.

One name sits at the centre of the silver short. JPMorgan absorbed the collapsing Bear Stearns in March 2008, in a deal brokered by the Federal Reserve, and inherited its silver short position, going on to become the dominant short in the COMEX silver market in the years that followed. None of this began with the futures market: governments were managing the gold price directly long before COMEX existed.

Confiscation, suppression, and a declassified cable

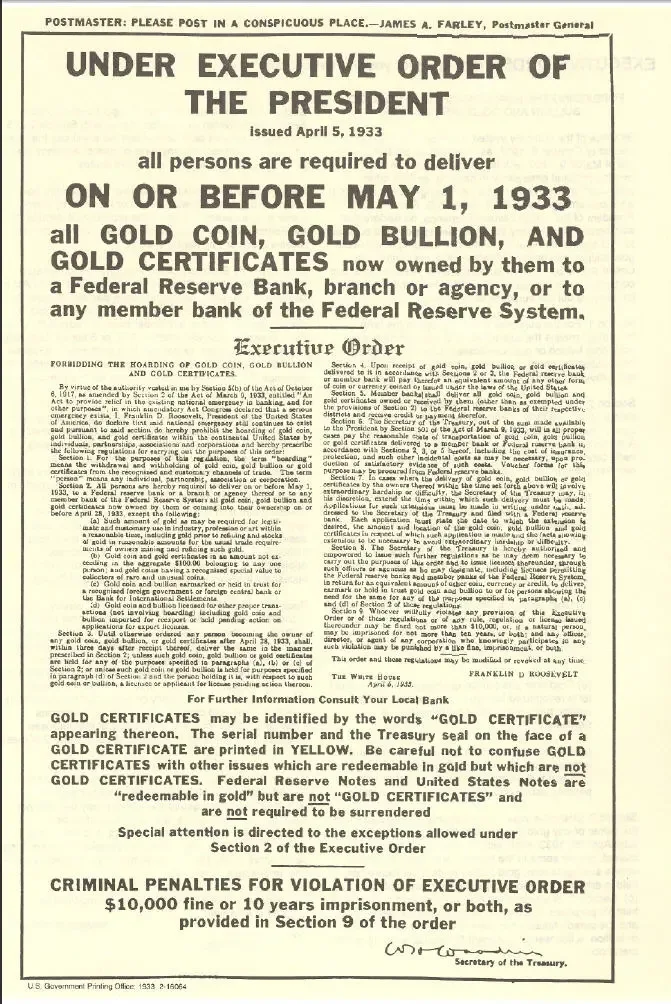

Confiscation: Executive Order 6102

On 5 April 1933, owning gold became a crime in the United States. President Franklin D. Roosevelt signed Executive Order 6102, which required every person in the country to hand over their gold coins, bullion, and gold certificates to a Federal Reserve bank by 1 May, in exchange for $20.67 an ounce. Holding gold beyond a small exemption was punishable by up to ten years in prison and a fine of $10,000, the equivalent of roughly $249,000 today. Americans surrendered about 2,665 tonnes.

Enforcement was real. Frederick Barber Campbell, a New York lawyer, was prosecuted after trying to withdraw the gold he had deposited at Chase National Bank. A San Francisco jeweller, Gus Farber, was prosecuted for selling thirteen gold coins, and a man named Louis Ruffino was sentenced to six months in jail and fined $500 for holding 78 ounces.

Less than a year later, the Gold Reserve Act of 1934 revalued gold from $20.67 to $35 an ounce, a 69% increase. The Americans who had handed over their gold at the lower price were paid in dollars the same government then devalued against gold. The revaluation created a paper profit of about $2.8 billion, and it went to the Treasury.

Private gold ownership then stayed illegal in the United States for more than 41 years. It became legal again on 31 December 1974.

Suppression: the London Gold Pool

From 1961 to 1968, eight central banks ran a coordinated operation to hold the gold price down. On 1 November 1961, the United States, West Germany, the United Kingdom, France, Italy, Belgium, the Netherlands, and Switzerland agreed to pool their gold reserves and intervene in the London gold market to keep the price at or near $35 an ounce. When the price threatened to rise, the Pool sold physical gold to push it back down. The Bank of England ran the trading desk; the members coordinated through the Bank for International Settlements in Basel.

For the first few years the Pool was a net buyer, because the market price sat at or below $35. From late 1965 it became a net seller, and gold drained out. The cumulative deficit from late 1965 to March 1968 reached $3.69 billion. France broke ranks first. On 4 February 1965, President Charles de Gaulle used a press conference to attack the dollar's privileged position in the monetary system.

"The fact that many states accept dollars as equivalent to gold ... has enabled the United States to be indebted to foreign countries free of charge."

De Gaulle did more than talk. Between 1963 and 1966, France ran a secret operation, code-named Vide-Gousset, to repatriate its gold from vaults in New York and London; it is reported to have brought home some 3,313 tonnes. In June 1967 France formally withdrew from the Pool, and the United States had to absorb its share, raising the American contribution from 50% to around 59%.

The end came in a single week. On 8 March 1968 the Pool sold 100 tonnes in one day, against a normal daily volume of about five. Over the following week it lost roughly 1,000 tonnes. On 15 March the British authorities declared a bank holiday and closed the London gold market. The central banks then split the market in two: an official price of $35 for dealings between governments, and a free market price for everyone else. Three years later, on 15 August 1971, Nixon ended the dollar's convertibility into gold entirely.

Suppression: US Treasury gold auctions

When Americans were finally allowed to own gold again, the government began selling it into the market. Private ownership became legal on 31 December 1974. Six days later, on 6 January 1975, the US Treasury held its first gold auction, offering two million ounces. The selling resumed under President Carter, who authorised monthly auctions from May 1978 to support a weakening dollar. Between 1978 and 1979 the Treasury sold 15.8 million ounces in 19 monthly auctions.

The Treasury was open about its goal. It described one aim of the sales as furthering "the U.S. desire to continue progress toward the elimination of the international monetary role of gold." A government that had just re-legalised gold was, in its own words, working to remove the metal from the monetary system.

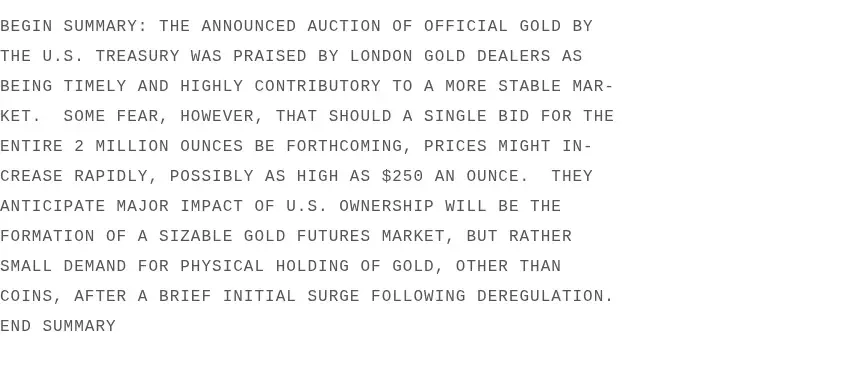

A declassified cable

Three weeks before private ownership became legal, the US Embassy in London sent a cable to Washington describing what the city's biggest gold dealers expected to happen next. Cable 1974LONDON16154_b, dated 10 December 1974 and signed by the embassy's deputy chief of mission, Ronald I. Spiers, recorded the views of four of the houses that set the London gold price: Samuel Montagu, Sharps Pixley, Mocatta & Goldsmid, and Consolidated Gold Fields.

The dealers told the embassy that the main effect of legal American gold ownership would be "the formation of a sizable gold futures market," with physical trading "miniscule by comparison." They were specific about what such a market would do to physical demand.

"Large-volume futures dealing would create a highly volatile market. In turn, the volatile price movements would diminish the initial demand for physical holding and most likely negate long-term hoarding by U.S. citizens."

A gold futures market opened on COMEX on 31 December 1974, the same day private ownership became legal. The dealers' forecast and the government's timetable matched: futures would dwarf the physical market, generate volatility, and discourage Americans from holding metal for the long term.

The cable does not prove the government built the futures market in order to suppress demand for physical gold. What it shows is foreknowledge. Three weeks before the launch, officials had been told in writing that a futures market would overshadow physical trading and dampen long-term holding, and they opened that market on the same day gold became legal. The document was classified at the time. It is a US government record, it has been declassified, and anyone can read it.

The short sellers who wrote the rules

Nine of the 23 members of the COMEX board held net short positions in silver during the winter of 1979 to 1980, totalling about 75 million ounces. That board voted on the emergency rule changes that forced silver's buyers to sell. The detail comes from a Fortune investigation published at the time, headlined "Who guards whom at the Commodity Exchange?"

The setting was the silver run of 1979 to 1980. The Hunt brothers, Nelson Bunker Hunt and W. Herbert Hunt, had built enormous long positions in silver futures and physical metal, and the price climbed from about $6 an ounce at the start of 1979 to nearly $50 by January 1980. Then the exchange changed the rules.

On 7 January 1980, COMEX adopted Silver Rule 7, placing heavy restrictions on buying silver on margin and cutting the most any trader could hold to 2,000 contracts, around ten million ounces, down from 5,000. Anyone above the new limit had to liquidate the excess by mid-February. Two weeks later, on 21 January, COMEX and the Chicago Board of Trade went further and suspended normal trading in silver futures, accepting liquidation orders only. Existing longs could sell. No new buy orders were taken. The single exception was that short sellers could still sell in order to make delivery.

Every one of these changes pointed the same way. They restricted buyers and left short sellers free to operate. The market became one-way: longs could only head for the exit, the price fell, and the shorts collected.

Two of the conflicted board members were named. Henry Jarecki chaired the COMEX margin committee and also chaired the silver dealer Mocatta Metals Corp; he was described as "a veteran of many silver deals with the Hunts." Asked about the conflict, his lawyer advised him to "use good business judgment." Mocatta posted "a banner first quarter in 1980" after the rules changed. Norton Waltuch, a vice president at ContiCommodity Services, was believed to have made more than $10 million personally as silver crashed.

At the Chicago Board of Trade, the chairman, Ralph Peters, disqualified himself from voting on the rule changes because of his own conflicts. No equivalent recusal was recorded at COMEX. The Hunts' attorneys later demanded the release of COMEX meeting minutes, in their words, "to determine if the members who were short disqualified themselves from the voting."

W. Herbert Hunt made the same point under oath. Before a U.S. House subcommittee, he named it directly:

"There were members of the Comex board who did have a vested interest in seeing that the price of silver went down. These were representatives or employees of major precious metal dealers, or floor brokers who had acquired short positions."

Silver did go down. It peaked near $50 in January 1980, collapsed through the spring, and by 1982 the London Silver Fix had fallen 90% to $4.90. The day of the steepest fall, 27 March 1980, is still known as Silver Thursday.

The pattern repeats

The same tool reappeared in 2011, when silver climbed from about $9 in the depths of the 2008 crisis back toward $50 by late April. Between 26 April and 9 May 2011, the CME Group raised the margin required to hold a COMEX silver futures contract five times in nine days. The margin on a single 5,000-ounce contract, for speculators, went from $11,745 to $21,600, a rise of about 84% in the cost of holding a position. On at least one occasion the CME announced two increases at once, one effective on a Thursday and the next the following Monday.

The price followed. Silver peaked near $49.85 on 28 April. By 5 May it had fallen to $34.95, a drop of about 30% in a week, and it did not trade above $30 again for nearly a decade. The CME described the increases as routine, made "as part of the normal review of market volatility to ensure adequate collateral coverage."

A margin rise applies to longs and shorts alike on paper, since both post the same collateral. In a rising market it falls hardest on the longs. They are the ones who must find more cash to stay in, and the ones forced to sell when they cannot, and that forced selling pushes the price down in the shorts' favour.

The gold market got the same treatment that year. When gold reached about $1,900 an ounce in the late summer of 2011, the CME raised gold margins 21% on 23 September to $11,475 per 100-ounce contract, part of a rise of roughly 90% over the preceding months. When the Reddit group WallStreetBets tried to push silver higher in late January 2021 and the price jumped 12.8% in three trading days, the CME raised silver margins again. In the 2025 to 2026 rally, with gold at record highs and silver above $80, it raised them once more, lifting gold margins from 6% to 8% of contract value and silver margins from 11% to 15%, and then to 18%.

The direction is always the same

These were not isolated decisions. Set the interventions side by side and the direction is consistent.

| Year | Intervention | Works against |

|---|---|---|

| 1980 | COMEX Silver Rule 7, margin restrictions | Buyers |

| 1980 | COMEX liquidation-only orders | Buyers |

| 2011 | CME silver margin hikes, five in nine days, +84% | Buyers |

| 2011 | CME gold margin hikes, about 90% over months | Buyers |

| 2021 | CME silver margin hike during the WallStreetBets squeeze | Buyers |

| 2025-26 | CME gold and silver margin hikes | Buyers |

The research found no example running the other way. No exchange was found raising margins to discourage short selling during a price decline, imposing liquidation-only orders on shorts during a crash, setting position limits aimed at short-side speculators, or making any rule change designed to arrest a rapid fall in the metal price. The CME's stated reason, managing volatility, would apply just as well to a market falling fast as to one rising fast. The tool comes out only when the price is going up.

The five-year investigation that found nothing

The Commodity Futures Trading Commission spent five years investigating whether the silver market was rigged. Its enforcement division logged more than 7,000 staff hours, working through position data, trading records across the physical, swaps, options and futures markets, and witness interviews. In September 2013 it closed the case. The agency announced it had found no basis to charge anyone.

The inquiry opened in September 2008, after complaints that large short positions in COMEX silver futures were holding the price down. It closed on 25 September 2013 with a statement that left no room for interpretation: there was "not a viable basis to bring an enforcement action with respect to any firm or its employees" in the silver markets.

Seven years later the same agency reached the opposite conclusion. In September 2020 the CFTC, alongside the Justice Department, established that traders on JPMorgan's precious metals desk had run a spoofing scheme in gold, silver, platinum and palladium futures from 2008 to 2016. The conduct ran straight through the years the CFTC had spent investigating and found nothing. The body that signed the 2020 order was the same one that had closed the silver file in 2013.

At least one person inside the agency had said so at the time. Bart Chilton, a CFTC commissioner from 2007 to 2014, stated publicly in October 2010 that he believed the silver market had been manipulated.

"Based on what I have been told by members of the public, and reviewed in publicly available documents, I believe violations to the Commodity Exchange Act have taken place in silver markets and that any such violation of the law in this regard should be prosecuted."

He held the position for years. In August 2012 he said there had been "devious efforts related to moving the price of silver." When the case was closed in 2013 he called it "not been a more frustrating nor disappointing non-policy-related matter at the CFTC." He was a sitting member of the commission, and he could not move it.

The frustration had a specific origin. In early 2010 a London metals trader named Andrew Maguire approached the CFTC with what he said was evidence of manipulation. On 3 February 2010 he sent the commission a written warning that a coordinated sell-off in silver was coming. Two days later, on 5 February, roughly 45,000 silver contracts were sold in the pattern he had described. Maguire went public that April, naming JPMorgan and HSBC. The CFTC closed the case three years after that.

Ten years to write one rule

The 2010 Dodd-Frank Act ordered the CFTC to cap how large a speculative position any single trader could hold in commodities including gold and silver. The point of a position limit is to stop any one player from getting big enough to move the price on its own. The CFTC wrote the rule. The banks went to court.

On 2 December 2011 two industry bodies, the International Swaps and Derivatives Association and the Securities Industry and Financial Markets Association, sued to block the limits, arguing they would reduce liquidity and increase volatility. In September 2012 a federal court vacated the rule and sent it back to the agency. The CFTC proposed new versions in 2013 and twice in 2016. None became law.

The final rule arrived on 15 October 2020, a full decade after the mandate. Chairman Heath Tarbert said it removed "a cloud that has hung over both the CFTC and the derivatives markets for a decade." For the metals contracts, the rule imposed federal limits only in the spot month; for every other month it deferred to limits set by the exchanges themselves. The two trade groups that delayed the rule for ten years counted among their members the banks that were, across the same decade, paying fines for manipulating the markets the limits were meant to protect.

The revolving door

The people who write and enforce these rules often came from the banks, or left to join them. A Reuters investigation found that 50 CFTC staff met with representatives of the top five banks more than ten times between 2010 and 2013. At least 25 of them later went to work for those banks, or for the law firms that represent them.

The pattern ran to the top of the agency. Jill Sommers sat as a CFTC commissioner from 2007 to 2013. Before that she had lobbied for the CME and run government affairs at ISDA, the same body that would later sue the CFTC to kill its position-limit rule. Gary Gensler chaired the CFTC after eighteen years at Goldman Sachs, where he had made partner. The commissioner who came from the exchange and the chairman who came from the bank now regulated the markets their former employers traded in.

Chilton took the same path out. The commissioner who had said the silver market was manipulated left the CFTC in 2014 and joined the law firm DLA Piper, where he advised a high-frequency-trading group he had criticised from the inside. The regulators are only part of the structure: the central banks at the centre of it hold their own gold beyond the reach of any comparable audit.

Fort Knox was last audited in 1953

Fort Knox holds the largest share of the United States gold reserve, and the last time that reserve was subjected to a comprehensive audit was 1953, in the first year of the Eisenhower administration. Even that exercise was partial, a spot check of roughly 6% of the metal, prompted by public rumours that the reserves had been drained to pay for the Second World War and Korea. The country claims 8,133 tonnes in all, more than any other nation, held across Fort Knox and three other depositories.

What has happened since is inventory, not audit in the sense an outside accountant would use the word. The Treasury's Office of Inspector General runs an annual procedure built around the Official Joint Seal: inspectors confirm that the seals on the vault compartments are intact, rather than opening them, counting the bars, and assaying the metal. Once a compartment has been counted and sealed, the routine narrows.

"the annual [audit] will be limited to inspection of the Seals."

The government's position is that the gold is all there. In 2011, Inspector General Eric Thorson told Congress that "100 percent of the U.S. Government's gold reserves in the custody of the Mint has been inventoried and audited," with all 42 compartments covered by the end of fiscal year 2008. The assay reports behind that statement covered about 3% of the reserve. KPMG, the external auditor, has never weighed or assayed the gold itself, and has said its opinion rests solely on the Inspector General's work; most audit papers from before 2004 have since been destroyed under records-retention rules.

The bookkeeping is its own curiosity. The Treasury still values the reserve at $42.22 a fine troy ounce, the statutory figure set in 1973, while the same ounce sells for around $3,300 on the open market. At the market price the hoard is worth more than $800 billion; on the government's books it is recorded at a small fraction of that.

In February 2025 the matter briefly reached the White House. President Trump said, "We're going to open up the doors. We're going to inspect Fort Knox," and Elon Musk, then leading the Department of Government Efficiency, wrote that "Maybe it's there, maybe it's not." Treasury Secretary Scott Bessent replied that "We do an audit every year. All the gold is present and accounted for." No visit took place, and by late May the Washington Times reported that the gold rush had fizzled.

Gold that has been lent out still counts as gold in the vault

The opacity is not confined to Washington. Most central banks report their bullion under a single balance-sheet entry, "gold and gold receivables," which folds metal physically held in the vault together with metal that has been lent to someone else. The Eurosystem's consolidated balance sheet for 31 December 2024 carried EUR 872,156 million on that one line, with no public breakdown between bars in storage and claims on bars that have left it.

Leasing is what fills the receivables half. A central bank lends physical gold to a bullion bank, which usually sells the metal into the market and owes the same quantity back when the term ends. Under IMF accounting rules the lent gold stays on the lender's books throughout, so the same bar can appear on two monetary authorities' balance sheets at once and be counted twice in the world total.

The amount of gold out on loan is not disclosed. Industry consensus put the peak at around 5,000 tonnes in the late 1990s and early 2000s; the analyst Frank Veneroso estimated far more, between 11,800 and 13,800 tonnes. The one public gauge of strain in this market, the Gold Forward Offered Rate, was withdrawn by the LBMA in January 2015, after it had turned negative during 2013 and 2014, a reading that points to physical scarcity. The reason given was limited usage and poor liquidity.

Germany planned seven years to bring its own gold home

Germany owns the world's second-largest reserve, about 3,350 tonnes, much of it stored abroad since the Cold War. When the Bundesbank decided to bring part of it home, it set out a timetable in January 2013 to move 300 tonnes from the Federal Reserve Bank of New York and 374 tonnes from Paris to Frankfurt by 2020, a seven-year schedule for the return of metal it already owned. In the first year, 5 tonnes arrived from New York.

The treatment of the returned bars raised a separate concern. The Bundesbank melted down and recast 55 tonnes of the gold, on the stated grounds that the bars did not meet the London Good Delivery standard. Recasting destroys the original serial numbers, the one marker that links a returned bar to the bar that was deposited, and the bar list the Bundesbank later published left out the refiner, the serial number, and the year of manufacture. Peter Boehringer, who later chaired the Bundestag's budget committee, was among those who pressed the question while the transfer was under way.

A contrast was available the whole time. In November 2014 the Dutch central bank moved 122.5 tonnes out of the same New York vault within weeks, and announced it only once the operation was complete. The Bundesbank, for its part, finished its own transfer in 2017, ahead of the published 2020 deadline.

Central banks are buying at the fastest pace since 1950

The institutions that hold these reserves have been net buyers of gold every year since 2010, reversing decades in which Western governments sold. Britain's disposal of about 395 tonnes between 1999 and 2002, at prices near $275 an ounce, became the emblem of the selling era; the metal raised roughly $3.5 billion then and would be worth more than ten times that now. Since 2010 central banks have bought more than 7,800 tonnes, and the rate has climbed rather than eased.

The recent totals stand well above the longer-run average. Between 2010 and 2021 central banks added around 473 tonnes a year, and then the pace roughly doubled.

| Year | Net central bank purchases (tonnes) |

|---|---|

| 2010 to 2021 average | about 473 per year |

| 2022 | 1,082 (highest since 1950) |

| 2023 | 1,037 |

| 2024 | about 1,045 |

| 2025 | 863 |

Figures from the World Gold Council and Visual Capitalist. The totals combine purchases reported to the IMF with the Council's estimate of the larger unreported flow.

The buying is led from outside the Western core. Poland was the largest single buyer in both 2024 and 2025 and now holds more gold than the European Central Bank. More than half of it goes unrecorded at the time: the World Gold Council estimated that about 57% of central bank purchases in 2025 were never publicly reported. By late 2025 the official world total stood near 36,500 tonnes, about 17% of all the gold ever mined, and gold had passed the euro to become the second-largest reserve asset in the world behind the dollar.

The behaviour is hard to reconcile with the official line on gold. The same institutions that ran the London Gold Pool, leased metal into the market, and sold reserves near the lows are now the most committed buyers of physical gold, accumulating on their own balance sheets the one asset that cannot be printed or written down by anyone else.

China reports one figure and is estimated to hold another

China's published reserves are large, and independent analysts who track the metal's movement put its true holdings well above the official figure. The People's Bank of China reported 2,322 tonnes as of April 2026, about 9% of its foreign reserves.

Jan Nieuwenhuijs, who has set out the most detailed public methodology, estimates Chinese monetary gold at roughly 5,411 tonnes by the third quarter of 2025, more than double the reported amount, and attributes about 80% of the world's unreported central bank buying to Beijing. China's own disclosure record makes quiet accumulation credible. In June 2015 the central bank announced holdings of 1,658 tonnes, up from the 1,054 tonnes it had last reported in 2009, a rise of more than 600 tonnes that had plainly been acquired over years of public silence.

The rules now treat vaulted gold as cash

The regulators who write bank capital rules place physical gold in the top grade. Under the Basel framework, allocated physical gold held in a bank's own vault carries a zero risk weight, the treatment given to cash and government bonds, the highest quality of capital a bank can hold. Gold has carried that weighting since the first Basel Accord in 1988.

Basel III, phased in across 2021 and 2025, sharpened the line between metal and paper. It removed the option, used in some countries under the earlier rules, to push gold down into the lowest tier of capital, leaving allocated physical bullion unambiguously alongside cash. At the same time its Net Stable Funding Ratio attached an 85% funding charge to gold positions, a cost that falls hardest on unallocated gold, the paper claims that make up most of London's trade.

One claim about these rules that circulates widely is incorrect. Basel III did not make gold a "Tier 1" high-quality liquid asset; the LBMA, which oversees the London market, has stated that no such reclassification was made or is expected, and gold remains outside the liquid-asset buffer banks hold against short-term stress. The change the rules made is narrower, and it still runs one way: a bar of metal in the vault is treated as the equal of cash, while a paper claim on gold is treated as a liability to be funded and discounted. The institutions closest to the monetary system keep their safest classification for the metal itself.

When the paper price stopped matching reality

On 19 March 2020 the price of silver fell below $12 an ounce, an eleven-year low. The same week, anyone who tried to buy a silver coin watched the price move the other way. An American Silver Eagle, which normally sold for about $3 over the spot price, now cost $9 to $11 over spot. The paper price said silver was collapsing; the price to hold an ounce of it in your hand was climbing.

What was being sold in March 2020 was futures contracts, not coins. As lockdowns spread, institutions dumped metal alongside everything else to raise cash, and gold briefly fell below $1,500. As the futures price dropped, the physical market seized in the opposite direction. A $1,000 face bag of pre-1965 US silver coins that had traded around 3% over its melt value in early March sold for $17,800 by the end of it, about 70% over spot. Generic rounds and bars were unavailable at any price, and where they could be found, premiums ran 50% to 100%.

Dealers could not keep pace. SD Bullion, on 24 March, said it had just taken more orders than at any time in its history.

"Last week, we received the most orders in the history of our company."

The mints ran dry at the same time. The US Mint temporarily sold out of 2020 Silver Eagles, the Royal Canadian Mint exhausted its Silver Maple Leaf stock, and in April the US Mint shut its West Point facility after COVID cases among staff. SilverGoldBull told buyers to expect shipping delays of twenty business days or more.

The COMEX gold market needed a new contract overnight

Behind the retail scramble, the wholesale market was failing in a more basic way. On 23 March 2020, bullion banks in London failed to deliver gold against Exchange for Physical transactions, the trades that tie the COMEX futures price in New York to the spot price in London. The two prices, normally within a dollar or two of each other, pulled apart. On 24 March, COMEX gold futures traded more than $80 above London spot, and bid-ask spreads in the spot market ran past $100.

The exchange responded by changing the product. On 24 March, CME Group launched a new futures contract, Gold (Enhanced Delivery), ticker 4GC. The existing gold contract could be settled only with 100-ounce bars; the new one accepted 400-ounce and kilo bars, widened the list of approved refiners from 68 to 252, and allowed delivery from vaults in London rather than New York alone.

Physical metal then moved to cover the gap the failure had exposed. On the first delivery day at the end of March, 17,302 contracts stood for delivery at once, equal to 56% of all the registered gold in the COMEX warehouses. Over the following months the New York vaults absorbed 732 tonnes of gold, between 24 March and 30 June 2020, close to quadrupling their holdings from 272 tonnes to 1,004 tonnes.

2011: the shortage was in coins, not metal

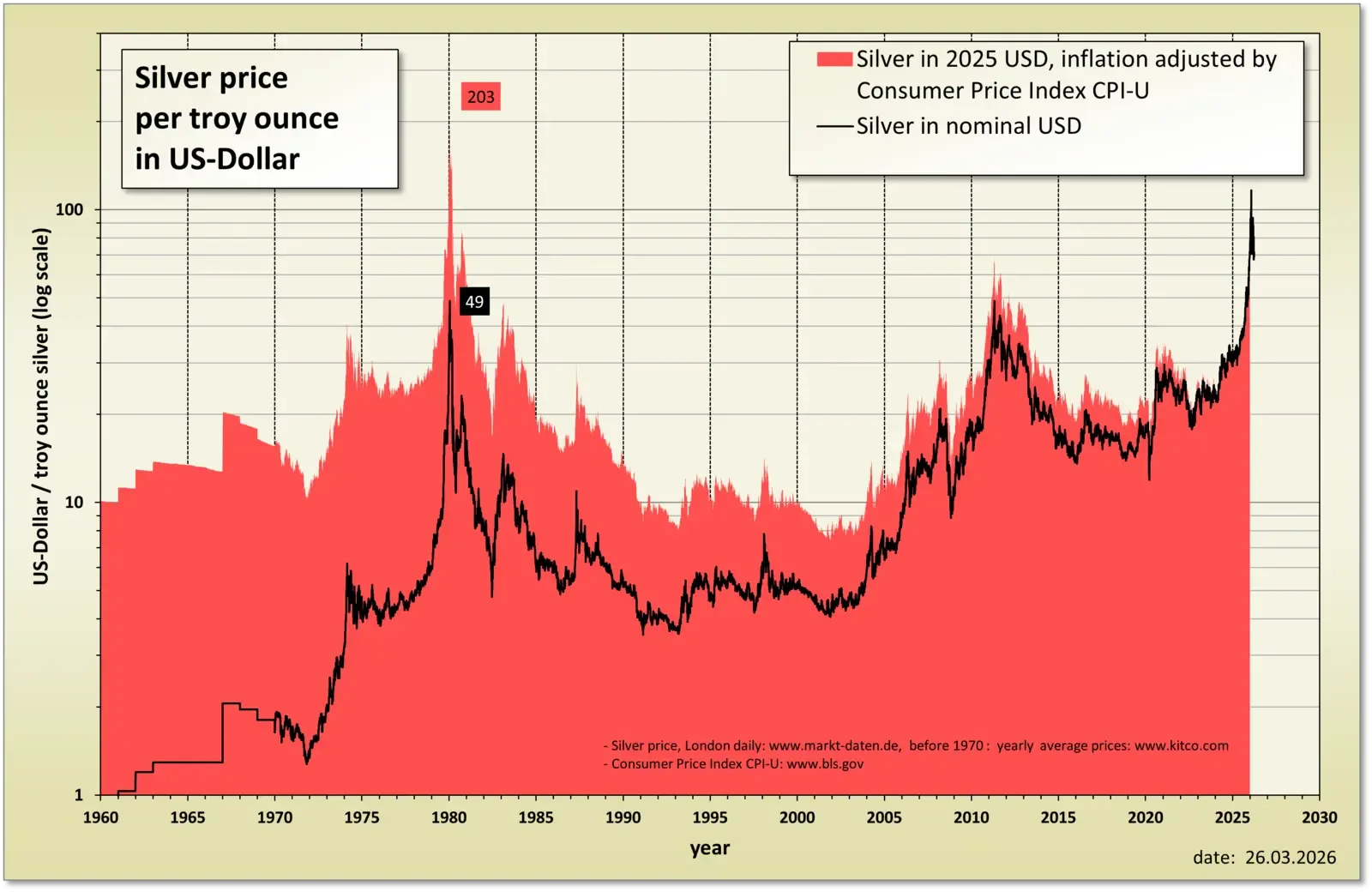

Silver ran from about $18 an ounce in the middle of 2010 to $49.82 on 25 April 2011, a gain of more than 170% and a 31-year high. The retail premium rose with it. American Silver Eagles changed hands at $8 to $10 over spot during the run, against a normal $3 to $4.

The shortage had a specific shape, and it was not a shortage of silver. The wholesale metal was there; the finished coins and small bars buyers wanted were not, at least not quickly enough. BullionVault, which trades large bars, reported "no shortage of the more common 0.999 bars," only "a shortage of immediate supply of higher purity 0.9999 fine silver" and fabricated product. The rally later turned and fell back, but the split was already on view: the paper price and the price of a coin in hand could separate by a wide margin while the vaults stayed full.

2021: a retail squeeze that moved metal but not the price

In late January 2021, fresh from the GameStop short squeeze, the r/WallStreetBets community turned to silver. The plan was to buy the SLV silver ETF in volume and force the paper shorts to cover. Silver topped $30 on 1 February 2021, an eight-year high, before settling back within two weeks.

The buying was real and large. In a single day SLV created 37 million new shares, which required purchasing an estimated 1,150 tonnes of silver, and it drew close to $1 billion in a session. Across the first quarter of 2021 the trust issued 176.7 million new shares. The physical market tightened in step: APMEX said it could not accept new orders on many products, and premiums on American Silver Eagles reached 34% to 38% over spot against a normal 12% to 15%, with some products carrying 75%.

The campaign was disputed inside the forum that supposedly drove it. Posts with tens of thousands of upvotes insisted WallStreetBets had nothing to do with the silver move, and that it was a distraction from GameStop pushed by funds that stood to gain.

"There is no silver short squeeze happening. NONE. NEVER."

No large short seller was forced to liquidate. Silver fell back, the premiums on coins slowly normalised, and the paper price ended roughly where it had started. The metal had moved; the price had not.

The Shanghai premium: the price where every contract delivers

The Shanghai Gold Exchange and the Shanghai Futures Exchange settle their contracts in metal, where COMEX historically delivers on less than 1%. When the Shanghai price sits above the COMEX or London price, the gap is called the Shanghai premium, and it tracks physical demand in the largest gold market in the world. For gold the premium normally runs $5 to $15 an ounce; above $30 is rare.

On 14 September 2023 it reached $121 an ounce, the highest on record since the exchange opened in 2002. The cause was policy. China's central bank had tightened gold import quotas to defend a weakening yuan, and with more than 60% of the country's gold supply coming from imports, the restriction created domestic scarcity on top of already strong demand.

| Period | Shanghai gold premium over the international price |

|---|---|

| Historical mean | about $6/oz |

| August 2023 average | $41/oz |

| September 2023 average | $75/oz |

| 14 September 2023 | $121/oz (record) |

The premium did not last. Once the import limits eased it subsided through 2024, returning to about $6 by August and briefly turning negative late in the year. Silver has held its premium more stubbornly. In December 2025 the physical silver premium in Shanghai ran above $8 an ounce, with metal on the exchange priced well over the COMEX futures.

The gap persists because of how the two markets are built. Shanghai requires delivery, import quotas set by the central bank can throttle supply, and capital controls on the yuan stop traders from arbitraging the difference away. When the premium is large and stays large, physical demand in the biggest market is outrunning what the Western paper price reflects.

The physical market keeps its own books. Silver has run a structural supply deficit every year since 2021, as industrial demand from solar panels, electronics, and electric vehicles has pulled more metal out of the market than mines and recycling have put back. The shortfall through 2024 came to roughly 678 million ounces, close to ten months of global mine supply. A futures price can be moved with a sell order. A deficit can only be closed with metal.

The premium is the one number the paper market does not set. It is fixed by what a buyer will pay and a seller will accept for metal that exists and can be delivered now. In March 2020, in 2011, and in Shanghai, the premium widened at the moment the futures price said metal was cheap or plentiful. The gap between the two prices is visible to anyone who has tried to buy a coin during a panic, and it has opened the same way each time these markets came under strain.

What bullion buyers should know

Every scheme and intervention set out in this guide pushed the price the same way. The spoofing desks talked about smashing it. Exchanges raised margins to break rallies and never to discourage shorting. Governments and central banks sold gold to hold the price down, not to lift it. The metal a buyer takes home is priced off that quote, so a price held below where a free market would set it reaches the buyer as a discount. The documented effect of the suppression, for the person buying a coin, has been a lower cost of entry rather than a higher one.

That is the part of the record that surprises people who arrive expecting the opposite. A buyer who suspects the price has been forced below its natural level is describing a discount to himself. The metal has been made cheaper to acquire, not dearer, by the very activity this guide documents, and a buyer who pays today is paying a managed price.

The premium is where the two markets meet

The number quoted on this site is the paper price. The number a buyer actually pays is that figure plus a premium, the margin a finished coin or bar carries over spot. The premium covers refining and minting, the dealer's costs, and distribution, and it moves with the balance of physical supply and demand at the moment of sale. In ordinary conditions it is small and steady. It is the one component of the price set by the market for real metal rather than by the futures exchange.

When the paper market and the physical market pull apart, the premium is where the strain appears. The quoted price can fall while the cost of an actual coin climbs, because the two numbers answer different questions. The futures price says what a contract is worth. The premium says what a bar in the hand is worth. The episodes set out earlier in this guide show that gap opening in full view, spot dropping at the very moment buyers found metal scarce, delayed, or unavailable at the published price.

None of this is advice on whether to buy, what to buy, or what to pay. It is a description of the ground a buyer stands on. The quoted price is managed. The banks that trade it most heavily have been fined and have admitted wrongdoing, and the central banks that oversee the monetary system are now among the most committed buyers of physical gold in the world, adding it to their own reserves while the paper price stays low. The premium, set by the trade in real coins and bars, is the part of the cost they do not control.

A coin in a drawer is not a contract. It cannot be cash-settled, rolled into a later month, or lent out and counted on two balance sheets at once. It is the asset itself, which is the one thing the paper market has never managed to reproduce.